This guidance provides information on the requirement to give effect to a section 107 direction under the Crown Entities Act 2004 (the Act), including monitoring and review. A step-by-step overview of the process for issuing and giving effect to a direction is provided below.

Steps and responsibilites in issuing a section 107 direction

Giving effect to a section 107 direction

Also under the Act, Crown entities subject to a section 107 direction must give effect [13] to the direction as soon as it comes into force. Note that under the Crown Research Institutes Act 1992 [14], Crown Research Institutes are only required to have regard to a section 107 direction.

Through consultation, or following implementation of a direction, entities may enquire about the on what that means for them. In addition to the requirements of the direction, it may be useful to advise Crown entities that under the Act, if applicable, it must:

- Give effect to or have regard to the direction, as the context requires (section 114) [15], as soon as it comes into force (see section 110) [16].

- Disclose in their Annual Report that they have been given a direction in writing in that year, and whether previous directions (relevant to them) remain in force (see section 151) [17].

- Amend their statement of intent and/or final statement of performance if the intentions and undertakings in either statement are significantly altered of affected by a direction (see section 148 [18] and section 149K [19]).

A full account of the activities affected by a requirement assists ministers, the Office of the Auditor-General and Parliament to understand where responsibilities lie for particular activities of the entity.

Monitoring the effectiveness of a direction

The initiating department for a direction is responsible for monitoring agency compliance with that direction, and obtaining required information to determine whether the intended benefits have been achieved.

As mentioned above, a direction can be most effective if consideration of how monitoring of compliance with the direction will occur and how achievement of the intended benefits will be assessed, is completed early in the development process. This helps to ensure that compliance and effectiveness with a direction can be appropriately and more easily monitored.

Review and expiry of directions

It is good practice for a direction to be reviewed before its specified expiry date, to determine whether it should be maintained. If a direction does not have a specific expiry date, the Act states that a direction must be reviewed after 5 years (section 115A) [20]. Further information around the consultation and notification requirements of such a review are also provided in section 115A of the Act.

Application of directions

Some directions involve extending the mandate of an agency with a leadership role over a particular system function or area (e.g. procurement) to Crown entities. Extending this mandate does affect the duties, responsibilities and operating model of a Crown entity board and its responsible minister.

As mentioned above, entities must include in some annual reporting documents any activities affected by a direction. This helps to assist ministers, the Office of the Auditor-General and Parliament to understand where responsibilities lie for particular activities of the entity.

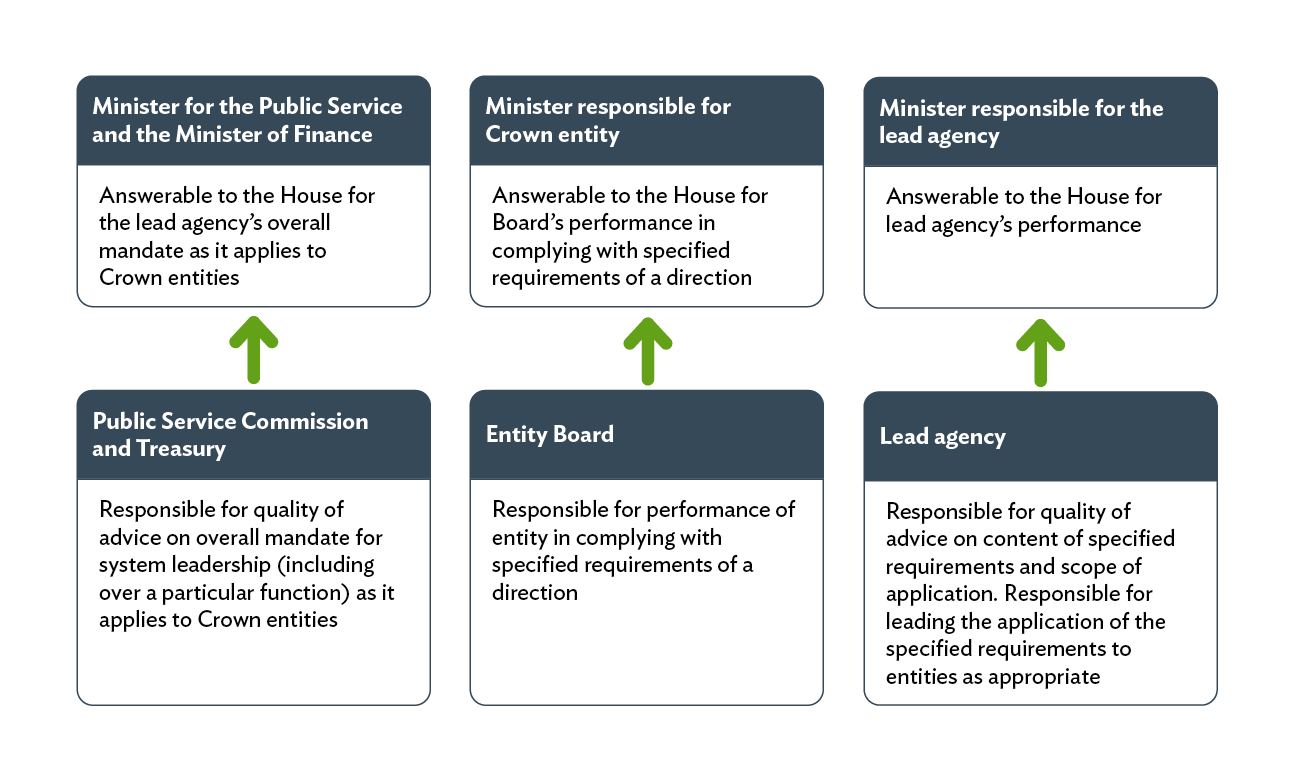

The diagram below shows what relevant ministers are answerable for, and the responsibilities of central agencies, Crown entity boards and agencies who are responsible for a particular system function.

[13]Section 107, Crown Entities Act 2004

[14]Crown Research Institutes Act 1992

[15]Section 114, Crown Entities Act 2004

[16]Section 115A Crown Entities Act 2004

[17]Section 110, Crown Entities Act 2004

[18]Section 151, Crown Entities Act 2004